http://www.guardian.co.uk/business/2012/mar/22/eurozone-crisis-portugal-strike-austerity

Just in - Ireland has fallen back into recession.

GDP data released at 11am GMT showed that GDP in the last three months shrank by 0.2%. That followed a 1.1% contraction in the third quarter of 2011 (revised up from a previous estimate of a 1.9% fall).

Ireland thus joins Greece, Belgium, Portugal, Italy, the Netherlands and Slovenia in recession.

Update:

Because Ireland is home to many international companies, it is also worth looking at its Gross National Produce (GNP), which discounts output from these firms.

But on GNP terms, Ireland is shrinking even faster. GNP fell by 2.2% in the fourth quarter of last year, following a 1.9% decline in Q3 2011.

In the bond markets this morning, Spanish debt has weakened - pushing the yield on its 10-year bonds above 5.5% for the first time since January.

Portuguese debt actually strengthened slightly, but with a 10-year yield of 12.6% the country is still being priced as a major risk.

Today's general strike comes as some economists and investors speculate that Portugal will need a second bailout.

Dutch finance minister Jan Kees de Jager touched on this issus this morning as he addressed the Netherlands' parliament

Dutch finance minister Jan Kees de Jager, last month. Photograph: John Thys/AFP/Getty Images

De Jager, who is one of the eurozone's more hardline finance ministers, told MPs that Portugal was "a different story" than Greece. True enough -- Portugal's problem, really, is that it has only managed very weak growth over the last few years.

Does that mean Portugal will not need fresh aid? De Jager was unclear on this point. He said that Portugal's fiscal programme agreed with the IMF was on track, but also cautioned that he could not rule out further debt restructuring within Europe (but wouldn't be drawn on Portugal specifically).

Earlier this week, my colleague Giles Tremlett reported that Portugal's health services has been hit by the austerity measures introduced since the country accepted a €78bn aid package.

Patients now face higher charges for services, and there is concern that this may have contributed to a rise in the mortality rate in February (although the government blames cold and flu outbreaks).

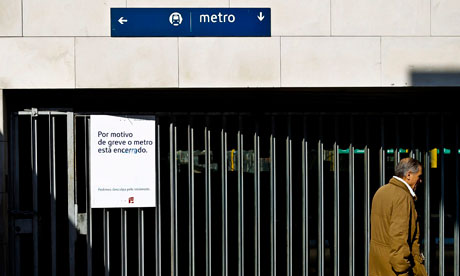

Word from Lisbon is that transport services have been badly hit by the general strike

From AP:

The Lisbon subway, which carries more than a half-million passengers every weekday, stayed closed. Train, bus and ferry companies in the capital and the second-largest city Porto provided only occasional services. Long traffic queues built up on roads into both cities as commuters resorted to their cars.

A man walks near a subway station informing about the general strike at Cais do Sodre Sstation in Lisbon, today. Photograph: Mario Cruz/EPA

http://www.zerohedge.com/news/overnight-sentiment-red-storm-rising-global-pmi-contraction

Submitted by Tyler Durden on 03/22/2012 07:11 -0400

Submitted by Tyler Durden on 03/22/2012 07:11 -0400

Flights are still operating at Lisbon's airport, though.

There are also reports that some schoolchildren were sent home, because teachers and auxiliary staff did not show up for work, and that some medical appointments have been cancelled.

GCPW, which called the strike (more details at 8.16am). has more than 600,000 members, mainly public sector and manual workers.

Just to add to the economic gloom, UK retail sales have suffered their biggest fall since last May. Sales volumes fell by 0.8% in February, compared with January.

January's figures, which were surprisingly good, have also been revised down sharply, to show growth of just 0.3%, not the 0.9% initially thought.

City analysts say this morning's poor PMI data (see 9.08am) is very disappointing. Here's a quick round-up:

Silvio Peruzzo of RBS:

It's a disappointing reading. It suggest that some of the optimism that was built in the last couple of months was overdone as far as the manufacturing sector is concerned for the big countries.

Howard Archer of IHS Global Insight

and...The Eurozone is far from out of the economic woods and is finding it hard to return to growth after GDP contracted by 0.3% quarter-on-quarter in the fourth quarter of 2011.

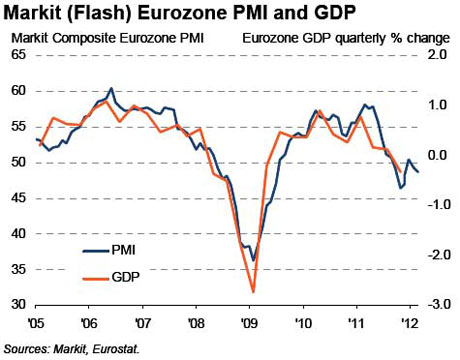

Indeed, the surveys reinforce our belief that it is more likely than not that the Eurozone will suffer further modest contraction in the first quarter of 2012 which will put it back into recession.You can see the full PMI data online here, in several European languages.The eurozone economy is weaker than thought, and heading into a full-blown recession.That's the message from this morning's purchasing managers' indexes (PMIs), covering the manufacturing and services sectors in March. They show that activity in both sectors fell sharply this monthThe flash manufacturing PMI for the full eurozone came in at 47.7, below the forecast of 49.5. Any number below 50 would indicate that the sector contracted. The flash services PMI fell to 48.7, from 48.8 in February.This meant the 'composite PMI', a combined measure of the euro economy, fell to 48.7 from 49.3 in February, showing activity fell more sharply.

As reported at 8.39am, the fall was driven by surprisingly poor performances in both France and Germany.Chris Williamson of Markit, which compiles the data, said the data showed that 2012 could be a very poor year for the eurozone. Having contracted in the last three months of 2011, it now looks very likely that GDP shrank in the current quarter too. Williamson said:The Eurozone economy contracted at a faster rate in March, suggesting that the region has fallen back into recession.As this graph shows, there is a clear correlation between the PMI data and GDP.The weak economic data from France and Germany (see 8.39am) has sent stock markets falling across Europe. Here's the details:FTSE 100: down 48 points, or 0.8%, at 5843.

French CAC: down 34 points, or 0.95%, at 3494

German DAX: down 60 points, or 0.86%, at 7010.Disappointingly data from France and Germany has raised fears that the eurozone's two largest economies are struggling.Both countries reported that their manufacturing output dropped this month, while their services data was also a concern.The French manufacturing PMI came in at 48.1, below the 50 point mark that seperates expansion from contraction (data via Markit), Economists had expected a repeat of February's 50.0 (which showed that output was flat).Germany posted a manufacturing PMI of 48.1, much worse than the 51.0 that was forecast. That's its first contraction in 2012.Chris Williamson, Markit economist, said the data raised fears that the debt crisis had been more damaging than thought, adding:While Germany may avoid a recession, it's growth is by no means robust. It's just scraping through.Seperate data showed that France's service sector was flat this month, with a PMI of 50.0, while Germany's came in at 51.8, down from 52.8 in February.

http://www.zerohedge.com/news/overnight-sentiment-red-storm-rising-global-pmi-contraction

Overnight Sentiment: Red Storm Rising On Global PMI Contraction

Futures continue exhibiting a very surprising and ever brighter shade of ungreen as the morning session progresses, starting with the 5th consecutive contractionary Chinese PMI data, going through disappointing European Manufacturing and Services PMIs which came below expectations (47.7 vs Est. 49.5 for Mfg; 48.7 vs Est. 49.2 for Services), with an emphasis on French and German PMIs, both of which were bad (German Mfg PMI 48.1, Est 51, prior 50.2; Services PMI 51.8, Est. 53.1, Prior 52.8), and concluding with UK sales which printed at -0.8% on expectations of -0.5%. And just like that Europe is "unfixed", prompting economists such as IHS' Howard Archer to speculate that following "worrying and disappointing" Euro PMI data, the ECB may cut rates to 0.75%, as Europe is finding it hard to return to growth after the Q4 contraction. And with that the beneficial impact of the €1 trillion LTROs is now gone, as Spain spread over Bunds has just risen to the widest in over 5 weeks, and the beneficial market inflection point passes - prepare for LTRO 3 demands any minute now.

European PMI chart from Reuters:

Sentiment summary from Bloomberg:

- First Word Cross Asset Dashboard shows sentiment down significantly on disappointing economic data from China to the U.K., with EU equities, risk FX significantly lower, Bloomberg analyst TJ Marta writes in following note:

- Most Asian equity indexes up moderately despite more contraction in Chinese PMI

- EU markets reacted significantly to disappointing GE, FR, EU PMI’s, as well as worse than expected decline in U.K. retail sales

- EU equity indexes down 1+ std. devs., led by CAC -1.5%; U.S. futures down ~1 std. devs., ~0.5%

- Bund, Treasury yields, curves down moderately to significantly

- JPY, USD outperforming on risk aversion

- Commodities lower, led by WTI -1.2%, copper -1.6%

- In sign that EU debt concerns continue, most EU sovereign yield to Bund spreads wider, with significant moves for Spain, Italy

And from BofA:

Market action

In Asia, financial markets finished mixed after Japan posted an unexpected trade surplus and the HSBC flash manufacturing PMI fell. The later helped boost speculation that the government may introduce further pro-growth policies. In India, the Sensex lost 2.3% while both the Shanghai Composite and the Korean Kospi lost 0.1%. On the flip side, the Hang Seng climbed 0.2% and the Japanese Nikkei increased 0.4%.

Weaker than expected overseas economic data - such as the Euro area flash PMIs - are causing a sell off in Europe and futures are pointing to a sell off in the US later today. In Europe, equities are trading down 1.3% in the aggregate. Blue chips are down even more off 1.6% while shares listed in London are off a smaller 1.0%. German and French listed firms are underperforming the broader market as well off 1.5% and 1.7% respectively. Here in the US, futures are pointing to a 0.6% lower opening for the S&P 500 later today.

In the bond markets, Treasuries are continuing to rally across the curve. The 10-year yield is currently 2.26% after falling 4bp. The risk off trade is sending yields on peripheral debt higher. The Spanish 10-year note is 7bp wider at 5.43%.

The risk off trade is boosting the dollar. The DXY index is up 0.2%. That is causing a sell off in commodities. WTI crude oil is $1.28 a barrel lower to trade at $106.00 and gold is off $13.38 an ounce to $1,637.25.

Overseas data wrap-up

The Chinese HSBC flash manufacturing PMI edged down to 48.1 in March from 49.6 in February. This is the first time in four months that the flash PMI has fallen. In our view, the flash HSBC PMI fell for two reasons. First, the HSBC measure focuses more on small and medium size businesses which are likely hit harder by tighter liquidity. Second, China's export manufacturers tend to be of small scale so the slowing in the global economy could have outsize impact on the flash HSBC PMI. Despite the weak PMI reading today we continue to expect the country's economy to expand by 8.3% to 8.5% yoy in the first quarter.

In Europe, the majority of the flash PMIs for the manufacturing and service sectors came in much weaker than expected in March. Consensus was looking for a pickup across the board but instead the PMIs fell sharply from their prior month's level. The headline Euro area manufacturing index dropped to 47.7 in March down from 49.0 in the prior month. The service sector PMI recorded a much a tiny drop from 48.7 from 48.8. The weakness was broad based with the Euro area's two largest economies Germany and France recording slippages in their PMIs. In particular, the German manufacturing PMI slipped to 48.1 in March from 50.2. The key takeaway from these reports is that the Euro area economy is not only contraction but the pace of contraction picked up in March. Our Euro area economists expect the Euro area's economy to contract by 0.5% yoy this year.

The UK retail sales report was disappointing. Retail sales ex auto fuel fell 0.8% mom in February. That was worse than the expected 0.5% mom drop penciled in by consensus. In addition, to February's weak reading the prior month's growth rate was revised lower by 0.6pp to 0.6%. Including fuel the retail sales dropped 0.8% mom in February and the prior month was also revised lower to show a 0.3% mom expansion instead of the previously reported 0.9% mom increase. The UK consumer is constrained by high unemployment, weak wage growth and a subdued economic backdrop. While retail sales is a volatile sub-component of overall consumer spending, this month's report does highlight the fact that we look for consumption growth to underperform the broader economy and only expand 0.3% yoy in 2012.

Eurozone industrial new orders fell 2.3% mom in January basically in line with market expectations of a 2.2% drop. The prior month's growth rate was revised sharply higher to +3.5% mom against an originally reported 1.9% increase. Looking ahead, we expect weakness in the Euro area's manufacturing sector; however, there will be pockets of strength notably in Germany where the manufacturing sector is geared to exports.

Tidak ada komentar:

Posting Komentar