http://globaleconomicanalysis.blogspot.com/2012/04/spain-would-be-dead-without-ecb-loans.html

Articles that appear in this blog translated from Spanish frequently appear in one of the major English news outlets a day or two later.

And so it is again.As a followup to my post Black Market in Spain: Cash Transactions Exceeding 2,500 Euros Now Banned The New York Times reports Spain Targets Tax Fraud To Counter a Recession.

The idea that banning 500 euro notes “bin Ladens” would accomplish anything is ludicrous. Moreover, as bad a the fraud is now, it is 100% guaranteed to get worse.

Unemployment is on the rise, and Spain is about to hike the VAT. With every tax hike comes more resistance to pay taxes. Spain is imploding and these measures will just make things worse. Please see Massive Jump in Bank of Spain Borrowing from ECB: Bank of Spain Balance Sheet Shows Spain Deep in Trouble, LTRO is Essentially Useless for more details.Get Money Out of Banks Now!

My advice to everyone in Spain: Take your money out of the banks while you still can. Capital controls are just around the corner.

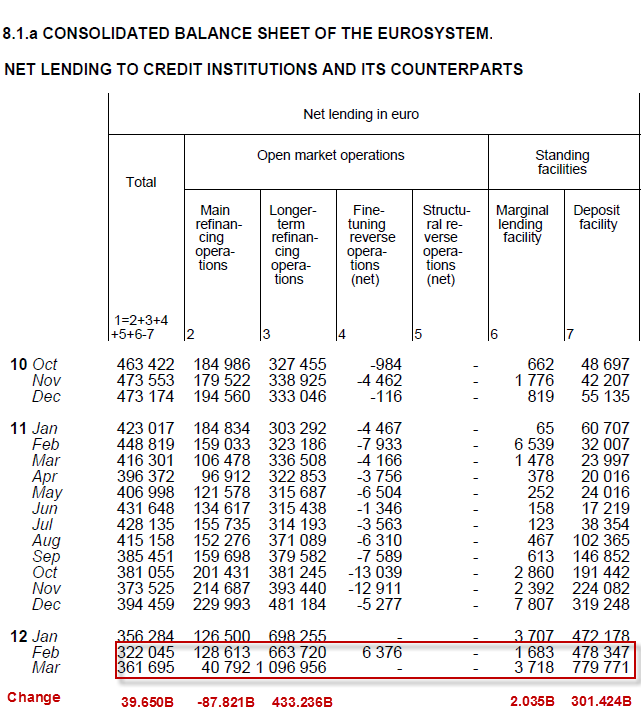

Inquiring minds are digging into Consolidated Balance Sheet of the ECB and by the Bank of Spain, searching for clues about the LTRO program for the entire Eurozone and also for Spain in isolation.

click on chart for sharper image

click on chart for sharper image

During March alone, the LTRO expanded by 433.236 billion but main refinance operations shrank by 87.821 billion. In March alone, 301.424 billion was parked right back with the ECB.

Please consider Spain.

ECB system-wide lending in March went up by 39.690 billion euros.

ECB lending to Bank of Spain alone jumped by 75.168 billion euros.

Thus, lending shrank by 35.478 billion euros elsewhere. What did Spanish banks do with the money? They parked it in sovereign bonds are now underwater on the purchases.

If you were looking for specific details as to why CDS rates for Spain hit an all-time high, there you have it.

Will There Be A ‘Corralito’ in Spain?

In response to Black Market in Spain: Cash Transactions Exceeding 2,500 Euros Now Banned, Gonzalo Lira pinged me with Will There Be A ‘Corralito’ in Spain?

Submitted by Tyler Durden on 04/13/2012 09:07 -0400

Submitted by Tyler Durden on 04/13/2012 09:07 -0400

"Spain Would Be Dead Without ECB Loans" Says Spanish Secretary of State for Economy; Update on Black Market Transactions in Spain; Bartering in Greece

As Greece wonders whether its debt crisis will eventually spell its exit from the euro, one town, Volos, has formed an alternative local currency as noted by the BBC in Greece Bartering System Popular in Volos.

A few months ago, an alternative currency was introduced in the Greek port city of Volos. It was a grass-roots initiative that has since grown into a network of more than 800 members, in a community struggling to afford items in euros during a deepening financial crisis.

From jewellery to food, electrical parts to clothes, everything here is on sale through a local alternative currency called TEM.

It works as an exchange system. If you have goods or services to offer, you gain credit, with one euro equivalent to one TEM.

You can then use your "savings" to buy whatever else is being offered through the network, leading to some rather original exchanges of goods.

It's all reminiscent of an ancient bartering system returning to today's Greece."Spain Would Be Dead Without ECB Loans"

"I can get language classes or computer lessons in return", says Stavros Ntentos from his stall where he sells children's underwear.

"It's a very good idea because we need to make people realise we can all buy and sell something; we don't only need euros."

"We can buy bread or meat in exchange for our products, or the girls can go to the hairdresser," says Peri Mantzafleri, who runs the co-operative.

"I grew up in a village - this was how it used to work in the old days, before money became involved. So this could be a chance to start again."

Articles that appear in this blog translated from Spanish frequently appear in one of the major English news outlets a day or two later.

And so it is again.As a followup to my post Black Market in Spain: Cash Transactions Exceeding 2,500 Euros Now Banned The New York Times reports Spain Targets Tax Fraud To Counter a Recession.

The Spanish government approved a number of measures on Friday to crack down on tax fraud as part of its efforts to reassure investors that Madrid can replenish the public coffers by bringing to the surface some of the country’s hidden wealth.

Jaime García-Legaz, the Spanish secretary of state for the economy, told the Spanish television channel laSexta on Friday that Spain “would be dead” without the loans provided by the European Central Bank.

To counter a deepening recession — the second in three years — the government of Prime Minister Mariano Rajoy is hoping to bring out some of the revenue buried in an underground economy that was estimated by the previous government to represent about 20 percent of gross domestic product.

The efforts to combat fraud come on top of a squeeze of 27 billion euros, or $35 billion, in the central government’s budget this year, as well as regulatory changes in labor markets and other areas.

As part of the measures approved at a cabinet meeting Friday, corporate cash transactions will be limited to 2,500 euros ($3,300), with fines as high as 25 percent of the transaction’s value levied upon any transfers above the limit. Individuals and companies will also face sanctions beginning next year for failing to declare all assets held overseas.

Use of 500 euro notes, worth about $657, is thought to have expanded considerably during Spain’s construction boom as a way of paying for large — and sometimes undeclared — property transactions or building materials. Spaniards came to call the 500 euro notes “bin Ladens”: everywhere and yet never seen.Banning “bin Ladens”Cannot Possibly Work

Cayo Lara Moya, leader of the United Left party in Spain, argued during a parliamentary session this week that the government should push for the complete removal from the euro zone of 500 euro notes, one of the largest denominations used in Western economies.

The idea that banning 500 euro notes “bin Ladens” would accomplish anything is ludicrous. Moreover, as bad a the fraud is now, it is 100% guaranteed to get worse.

Unemployment is on the rise, and Spain is about to hike the VAT. With every tax hike comes more resistance to pay taxes. Spain is imploding and these measures will just make things worse. Please see Massive Jump in Bank of Spain Borrowing from ECB: Bank of Spain Balance Sheet Shows Spain Deep in Trouble, LTRO is Essentially Useless for more details.Get Money Out of Banks Now!

My advice to everyone in Spain: Take your money out of the banks while you still can. Capital controls are just around the corner.

and...

http://globaleconomicanalysis.blogspot.com/2012/04/massive-jump-in-bank-of-spain-borrowing.html

Massive Jump in Bank of Spain Borrowing from ECB: Bank of Spain Balance Sheet Shows Spain Deep in Trouble, LTRO is Essentially Useless

CDS rates to protect against default by Spain rose to an all-time high today as Investors brace for more pain in Spain.

Spain was firmly back in the spotlight on Friday, after news of a sharp rise in borrowing by the region’s banks from the European Central Bank triggered losses across European stocks, but especially for the IBEX 35 index XX:IBEX -3.58% , which fell more than 3% to a three-year low.

The yield on the 10-year government bond in Spain ES:10YR_ESP +0.0004% , which had appeared to get some relief in the latter half of the week, resumed a climb upward, rising 15 basis points to around 5.93%.

The cost of insuring Spanish government debt against default using credit-default swaps, or CDS, rose to an all-time high. The five-year Spanish CDS spread widened to 505 basis points from 476 basis points on Thursday, according to data provider Markit.

That means it would now cost $505,000 annually to insure $10 million of Spanish government debt against default for five years.Massive Jump in Bank of Spain Borrowing from ECB

Data released by the Bank of Spain showed gross borrowing from the central bank hit 316.3 billion euros ($416.7 billion) in March, up from €169.86 billion in February.

Inquiring minds are digging into Consolidated Balance Sheet of the ECB and by the Bank of Spain, searching for clues about the LTRO program for the entire Eurozone and also for Spain in isolation.

Consolidated Balance Sheet of Eurosystem

Net Lending to Credit Institutions

Net Lending to Credit Institutions

click on chart for sharper image

click on chart for sharper imageDuring March alone, the LTRO expanded by 433.236 billion but main refinance operations shrank by 87.821 billion. In March alone, 301.424 billion was parked right back with the ECB.

Please consider Spain.

Consolidated Balance Sheet of Banco De Espana

click on chart for sharper image

ECB system-wide lending in March went up by 39.690 billion euros.

ECB lending to Bank of Spain alone jumped by 75.168 billion euros.

Thus, lending shrank by 35.478 billion euros elsewhere. What did Spanish banks do with the money? They parked it in sovereign bonds are now underwater on the purchases.

If you were looking for specific details as to why CDS rates for Spain hit an all-time high, there you have it.

Will There Be A ‘Corralito’ in Spain?

In response to Black Market in Spain: Cash Transactions Exceeding 2,500 Euros Now Banned, Gonzalo Lira pinged me with Will There Be A ‘Corralito’ in Spain?

The “corralito” (“little bullpen”) was when the Argentine government limited weekly transactions to AR$250 a week back in 2001.

In my piece, I argue that a “corralito” would be part of a Spanish withdrawal from the eurozone—and on cue, Rajoy is on the road to implementing it.

There is no solution to the Spanish problem except EMU exit and devaluation.Lira's target date for Spain exit from Eurozone this year is certainly debatable, but economically-speaking it is bound to happen as the current setup is extremely unstable and worsening every day.

and....

http://www.zerohedge.com/news/how-ecb-turning-spain-greece

How The ECB Is Turning Spain Into Greece

As Spanish CDS surge and bonds shrug off the very recent gloss of a 'successful' Italian debt auction, the sad reality we pointed out this morning is the increasing dependence between Spanish banks, the sovereign's ability to borrow, and the ECB. As ING rates strategist Padhraic Garvey notes this morning, the bulk of the LTRO2 proceeds were taken down by Italian (26%) and Spanish (36% of the total) and the latter is even more dramatic given the considerably smaller size of Spanish banking assets relative to Italy. The hollowing out of the Spanish banking system, via encumbrance(ECB liquidity now accounts for 8.6% of all Spanish banking assets), is a very high number - on par with Greek, Irish, and Portuguese levels around 10% where their systems are now fully dependent on the ECB for the viability of their banks. His bottom line, Spain is not looking good here and while plenty of chatter focuses on the ECB's ability to use its SMP (whose longer-term effectiveness is reduced due to scale at EUR214bn representing just 3% of Eurozone GDP), consider what happened in Greece! The ECB did not take a Greek haircut and so the greater the amount of Greek debt the ECB bought, the greater the eventual haircut the private sector was forced to take. By definition, every Spanish bond that the ECB buys in its SMP program increases the default risk that private sector holders are left with. Only outright QE, a promise not to default and a willingness to expand the ECBs balance sheet with ownership of the entire stock of Spanish debt if necessary (in the extreme) would be enough to cause a material positive effect from ECB intervention but it is clear from the massive compression in German yields (and weakness in Spain) that the market remains nervous amid an ongoing preference for core. Of course the cycle of crisis, as BNP noted, from crisis to complacency is becoming more chaotic and less sustainable.

* * * *

ECB dilemma / Bank liquidity

Latest central bank data (which comes out with a lag) shows that the 2nd 3yr LTRO was dominated by Spanish and Italian banks. Specifically we estimate that Spanish banks took down 36% and Italian banks took down 26% of the total. The larger takedown of Spanish banks here is significant as the size of its banking assets are lower than those of Italy, hence in proportional terms Spanish banks have shown the greatest need for 3yr LTRO cash.

On an on-going basis Spanish banks now take down some 316bn of ECB liquidity, which represents 8.6% of its banking assets. This is a very high number. By way of comparison Greek, Irish and Portuguese banks take down some 10% to 12% of their banking assets in ECB liquidity, and these systems are basically fully dependent on the ECB for the viability of their banks. Spanish banks are not far behind on this metric. The next worst are Italian banks with the liquidity takedown of 6.5% of their banking assets.

Bottom line, Spain is not looking good here. There has also been a warning shot aimed at Ireland from the ECB's Asmussen, who asserts that the current amount of liquidity support extended by the ECB and through ELA (additional liquidity support through the Irish Central Bank) "needs to be substantially reduced over time". He also warns that Ireland should be very careful on any deviation from the original promissory notes agreement, suggesting that any restructuring here should be preceded by reduced bank reliance on emergency liquidity assistance.

At the other extreme, Dutch banks take down a mere 0.4% of their banking assets in ECB liquidity, and latest data show German banks taking liquidity to the equivalent of 0.6% of their assets. We estimate that German banks took down 8% of the 2nd LTRO while the Dutch take down was significantly small. The French need for ECB liquidity is higher, with total ECB takedown running at 147bn, which represents 1.7% of its banking assets, and we estimate that French banks took down 12% of the 2nd 3yr LTRO.

In the past three weeks there has been evidence that the beneficial effects of the two 3yr LTROs are largely behind us, with spreads under widening pressure again. In the meantime there has been no evidence of ECB bond buying through its SMP program.While the SMP may be resumed and would have a positive impact, it could ultimately risk making things worse. Why? Consider what happened in Greece.The ECB did not take a Greek haircut. So greater is the amount of Greek bonds that the ECB bought, the greater was the size of the private sector haircut required in order to get to the 120% medium-term debt/GDP target.

A baseline assumption is that the same could happen in the future i.e. if there had to be, say a Spanish, restructuring (albeit unlikely) at some point in the future that the ECB would not share in the pain. By definition then, every Spanish bond that the ECB buys in its SMP program increases the default risk that private sector holders are left with. The SMP program has survived the Greek default event because the ECB did not take a haircut, but that action in itself has impaired the effectiveness of the SMP. Only outright QE, a promise not to default and a willingness to expand the ECBs balance sheet with ownership of the entire stock of Spanish debt if necessary (in the extreme) would be enough to cause a material positive effect from ECB intervention.

A more positive gloss has taken hold in the past few days, coinciding with Italy getting paper into the market yesterday amid a strong convergence theme for peripheral spreads to core. However, the fact that 2yr Schatz trade close to a single digit and that the 5yr area is trading so rich to the curve tells us that this market remains very nervous amid an ongoing preference for core.

Tidak ada komentar:

Posting Komentar